#443 | Busch v Pacific Life

Image: AP

It’s been a very long time since anything related to life insurance has broken into mainstream media. Larry King famously claimed to be scammed by a STOLI transaction that had been executed with his approval and paid him $1.4 million in 2007. The case was settled in 2008, but it drew an enormous amount of attention to STOLI and contributed to strengthened insurable interest laws that clamped down on the practice. Then there was the saga of Gene Simmons from KISS partnering up with Cool Springs to pitch premium financed IUL on Bloomberg back in 2010. The Wall Street Journal even ran an article on it. But aside from these two bizarre episodes, life insurance effectively never makes the news.

As of last week, we can add another one to the list. Two-time NASCAR Cup champion Kyle Busch and his prominent wife Samantha Busch went public with their lawsuit against Pacific Life claiming $8.5 million in damages from the purchases of several Indexed UL policies. The story is massive. All of the local Charlotte news stations covered it first, obviously, but so have Newsweek, Fox News, ESPN, Yahoo Sports, the AP and a host of motorsports publications. Googling Pacific Life fills the page with news results for the lawsuit. The saying goes that any press is good press. I’m not sure Pacific Life – or anyone in the life insurance industry, for that matter – would agree.

There are a lot of angles to the claims in the lawsuit. One is that the policies were positioned as “investments” that would deliver “tax-free retirement income.” That claim alone is problematic, particularly given that the language shows up in some of the emails that are included in the lawsuit, including from people at Pacific Life. Another angle is that the policies listed in the lawsuit are Pacific Discovery Xcelerator (PDX) and its successor, PDX 2. Both of those products have been the subject of several other lawsuits over their inherent risk, complexity and lack of transparency.

Either of these angles could be reason alone to litigate, but neither of them individually or together can explain the astonishing loss of $8.5 million on $10.9 million of premium paid over just 7 years. Permanent life insurance is a simple product. Premiums go in, policy charges go out, whatever is left over earns interest. Cash value is the balance of that equation. If the Busches lost $8.5 million on a product with a 0% crediting floor, then there is only one explanation for how that could have happened.

Therein lies the most problematic angle of all – that exorbitant agent compensation caused enormous policy charges that ultimately resulted in the losses. This case isn’t really about life insurance in general, Indexed UL in particular or PDX/PDX 2 specifically. It’s about the unique way that Pacific Life has approached agent compensation for the last 40 years and one agent who decided to push compensation to the absolute limit for his own benefit at the expense of policy performance.

Undoubtedly, critics of life insurance will say that this case is indicative of a normal policyholder experience. That is absolutely and unequivocally not the case. Life insurance policies used for accumulation and funded at the maximum non-MEC premium effectively can’t lapse – that’s literally how the maximum premium limitations are calculated. I own permanent life insurance policies and I overfund them. These policies do what they are supposed to do. Theoretically, the situation with the Busches should never have happened. And yet, it did.

How is that possible? The only way to know for sure is to see the as-issued illustrations. I have them. Those illustrations, combined with policy statements, paint the picture of exactly how this situation came to pass. There are still open questions, but one thing is clear – these policies were built to fail. This situation should never have happened. The experience that Kyle and Samantha Busch had with life insurance is, in no way, an indication of what is normal. But the fact that it did happen tells us that they are also assuredly not alone. And for that reason, we have to reckon with what this case shows us.

First, the basics. Both Samantha and Kyle Busch purchased PDX policies in 2018. Samantha’s remained in-force but Kyle’s was exchanged to a new PDX 2 policy in 2022. In 2020, Kyle purchased two additional PDX 2 policies, one with $44.5 million in death benefit and the other with $17.5 million. As a NASCAR champion with a long career ahead of him, Kyle was issued in 2020 at Super Preferred with a $4.92 Flat Extra per $1,000 of face amount for 20 years, reflecting the inherent risk of professional racing. For the purposes of simplicity, I’m going to focus all of the analysis on just the $44.5 million PDX 2 policy issued in 2020. It is indicative of the design of all the policies owned by the Busches.

The policy was configured in a way that anyone who is familiar with Pacific Life policies would immediately recognize as being problematic. The premium commitment from Kyle for this policy was $1.5 million per year for 5 years. I know that 5-pay designs are prevalent in the industry but, in my view, they are inherently inefficient. Section 7702A is set up to test on a 7-pay premium basis, which means that paying 7 years is almost always the most efficient way to maximally fund a policy. The caveat, as discussed in #394 | The Curious Case of the MassMutual 8 Pay, is that premium should be extended to 8 years for typical retail policies with per thousand charges, such as this one.

It would have been more efficient for this policy to have paid $1 million for 7 years and $500k for the 8th year while still retaining non-MEC status to ensure the lowest possible death benefit. According to the lawsuit, the point of this sale was “tax-free retirement income.” Death benefit for estate planning or income protection purposes was not mentioned. As a result, we can assume that the Busches were using these policies for the sole purpose of driving accumulation and income. Extra death benefit was not a goal.

And yet, this policy was issued with a stonking $44.5 million death benefit. That would be a problem for any normal policy meant to be overfunded, but particularly for one with a $4.92 Flat Extra per $1,000 of face amount. The total COIs including the Flat Extra tally to $2.26 million on PacLife’s currently sold Horizon IUL 2, which is virtually identical in design to PDX 2 and serves as a proxy for Kyle’s policy. Without the Flat Extra, the total COIs would have been just $181k. Extra death benefit is always suboptimal on accumulation designs. But here, it was catastrophic, sucking up over 30% of the paid premium in just the first 10 years.

Why did the agent set it up this way? We could, maybe, have given him the benefit of the doubt and said that it’s a good thing for a NASCAR driver to have extra death benefit coverage while he’s racing. I get that argument. That is, I’m sure, what the agent would argue in court. But nowhere does the desire for death benefit come up in the lawsuit. Instead, we know the game – more death benefit equals a higher Target premium. There is little justification for a death benefit this size other than increasing commission. It was well in excess of what was strictly needed to fit the premium flow into the policy for tax purposes.

The agent could have stopped there, but he didn’t. Rather than using commission-free ART Coverage for a portion of the $44.5 million in death benefit, the agent decided to use fully commissionable Basic Coverage for the entire amount. PacLife sets the default ART/Basic Coverage split at 50/50, which generally puts the commission to a level that is market-competitive. This policy was purposely configured to pay more than double market-competitive compensation with a 100% Basic Coverage design. As discussed in last week’s article, there is no legitimate benefit to using Basic over ART Coverage. It’s a commission play, pure and simple, that transfers value from the policyholder to the agent.

On top of that, the agent issued the policy with an Increasing DB in year 1 with a planned switch to Level DB in year 2. The charitable rationale is that the agent was trying to increase GLP/GSP limits, but that could have been easily handled by just using CVAT. The real reason, it seems, was to further increase compensation. By issuing the policy with Increasing DB rather than Level DB, the Target premium with a 100% Basic Coverage jumps from $550,910 to $1,494,310. It’s probably not a coincidence that the Target is just a hair off the planned premium of $1.5 million. You can imagine how this probably happened – Kyle and Samantha committed to $1.5 million and then the agent worked the policy to get the compensation to match. By every indication, that’s exactly what happened.

The incredible part of the story is that because these policies were issued prior to AG 49-A being enacted in 2021, they still illustrate remarkably well. This policy illustrated a whopping $787k in annual income (via indexed loans, of course) starting at age 51 and running to age 80. The IRR on both the income and the illustrated residual cash value at age 95 is 6.09%, which is above the illustrated rate of 5.76%. It’s easy to blame PDX and PDX 2 for this fiasco, but Horizon 2 IUL illustrates $626k of annual income with the exact same configuration. This same sale could have happened almost as easily last week with Horizon 2 IUL under AG 49-A as it did in 2020 with PDX 2 under AG 49.

This speaks to something of a truism in life insurance – commissions don’t matter if the illustrated rate is high enough and the illustration runs long enough. Time and performance always outweigh initial policy charges over the long-run. Unless Kyle and Samantha had been shown a properly designed policy, which they weren’t, they couldn’t have known that their policy configuration was flawed. The numbers still look good on the illustration if you just run your finger far enough down the ledger.

The real world, however, exists only in the short-run and that’s where these policies ran into problems. For every $1 of Target, there are roughly $2.6 in policy charges over the first 10 years of the contract. In this policy, that equates to around $3.85 million or just over 51% of total premium in charges over the first 10 years, using Horizon 2 IUL (Balanced) as the proxy. On top of that, every premium is assessed a 5.9% premium load, which totals $450k over the 5 years. Add all of those charges up including the COIs with the Flat Extra and you’re at $6.6 million, or 88% of premium.

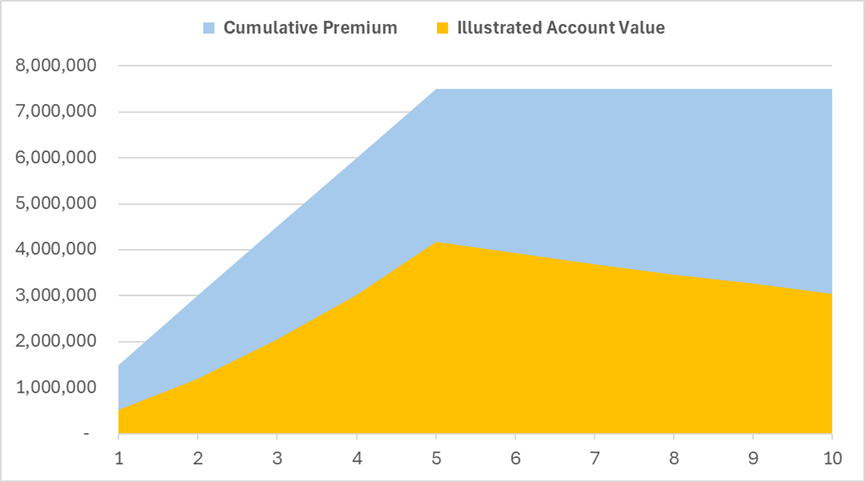

You can even see the effect of the charges in the as-issued illustrations at the maximum AG 49-A rate and allocated to the Performance Plus accounts. Take a look at the cash value decline that happens after the 5th year as charges overwhelm illustrated indexed interest credits. The gap by year 5 between Account Value and cumulative premium is a whopping $3.32 million and it grows to $4.5 million by year 10. After that, the coverage charges related to commissions burn off, the death benefit is illustrated to reduce to the minimum and the contract starts to grow in value.

The fact that charges overwhelm credits even on the original illustration is an indication of the fragility of the original design. Money has to get into a policy in order for it to persist. That only happens two ways – interest crediting and premium payments. Strong policy performance might have saved the day but the average policy interest crediting rate through February of 2024 was just 1.5%. How in the world is that possible? Because for the first three years of the policy, the cash value was allocated to the Fixed Account earning 2.25%. Once the reallocation happened, the performance of Indexed accounts was effectively zero. I have no words for this. Since 2020, the S&P 500 has rattled off 16%, 13%, -8%, 21%, and 21% returns on the 2/15 sweep date. Allocating to the Fixed Account meant that Kyle Busch got virtually none of it.

On top of that, the $1.5 million premium was billed semi-annually at $750k but was only paid annually, except for one July premium of $750,000. As a result, the total premium over the first 4 policy years was just $3.75 million against (estimated) policy charges of $4.15 million. So what happened to this policy? It lapsed. And so did the other PDX 2 sold in 2020 – and so did Samantha’s 2018 PDX, despite the fact that all of those premiums were paid and the policy performed at 6.1% through June of 2023.

It’s easy to point the finger at Kyle as the reason why the policies lapsed. Yes, he should have paid the full $1.5 million premium every year. If he had, the policies wouldn’t have lapsed, at least not yet. But the losses would still have been $8.5 million, if not more because of the 5.9% premium load and the Fixed Account allocation. These policies were doomed to fail. No contract should be set up to consume nearly 90% of the premium in policy charges over the first 10 years. No contract should be left to die in a Fixed Account yielding 2.25% when more competitive indexed crediting options are available. There are a litany of errors that all contributed to the ultimate outcome, but none more egregious than a policy clearly configured to maximize compensation to the agent at the expense of the client.

This situation couldn’t have occurred with any other carrier, at least not at this magnitude. Could the agent have sold more death benefit than was strictly necessary with another carrier? Of course. But would the Target premium have been this high? Absolutely not. This agent could have sold any other carrier with the same $44.5 million Increasing DB and the Target would have been between $500k and $600k. But at PacLife, the agent could push the Target all the way to $1.5 million. That is exactly, precisely, and unambiguously the cause of this situation. Not life insurance. Not Indexed UL. Not even PDX. The problem is a compensation structure unique to Pacific Life that can create a situation like this.

The agent could just as easily have made a different choice to favor Kyle and Samantha Busch in the policy design. If the agent had sold the same cumulative premium but spread over 8 years with the minimum amount of death benefit, which at the time was around $32 million under the old 4% 7702 regime. He could have used a 50/50 Basic/ART Coverage blend with a level death benefit (using CVAT), the commission would have been right around $200k. The total Coverage Charges over the first 10 years would have dropped from $3.6 million to just $567k. Total policy charges would have dropped from 88% of total premium in the as-sold design to just 33%, the vast majority of which is related to the Flat Extra.

That policy configuration would have worked out perfectly well. The cash value would go up every year in the base illustration scenario. There would have been no massive loss on the ledger and no lapse, even if the premiums weren’t fully paid. In other words, this situation would have been entirely avoided by a quality policy design built in favor of the client, not the agent. The agent made a choice. It was a terrible one – but it was his choice.

Since this lawsuit has hit the press, I’ve heard from many agents. They all say basically the same thing. They’ve all seen cases just like this one. They’ve all seen 100% Basic Coverage designs. They’ve all seen aggressive illustration assumptions paper over egregious policy charges from exorbitant compensation. Many of these agents end with a variant on this statement: “…and that’s why I don’t sell Pacific Life.” They don’t want to feel as though they have to continuously fight against their own incentives in order to give more benefit to the customer. A lot of agents just don’t want to be put in that position. In other words, they don’t want to have to make the choice. I don’t blame them.

This is one case, one agent and one client. It should not be used to generalize across all life insurance policies, across all Indexed UL policies or even across all policies at Pacific Life. But it is an indication of what exists in the marketplace with Pacific Life policies. This lawsuit might look like it’s about life insurance being positioned improperly as an investment – and it is. It might look like it’s about hyper-aggressive illustrations on a uniquely complex and opaque Indexed UL product – and it is. But at its core, this lawsuit is about the effect of agent compensation on policy performance.

The irony is that the industry has nothing to hide when it comes to commissions. If anything, life insurance agents are underpaid over the life of the policy. Properly designing, underwriting and managing a life insurance policy over time is no cake walk. Selling life insurance is exceedingly difficult. But as I’ve written in many previous articles, upfront life insurance commissions are lower than typical advisor AUM fees over the life of a contract. Upfront commissions create an incentive for agents to do the initial hard work of selling a product that basically no one wants to buy.

The downside of upfront compensation is that it harms short-term performance in exchange for delivering better long-term values, at least relative to pure AUM-based fees. But as I said earlier, the long-term is theoretical. People only live in the short-term. And in the short-term, upfront commissions can create real problems in life insurance contracts. This case is an extreme example of how egregious upfront compensation can undermine the core premise of what a life insurance policy is supposed to do. It literally destroyed a plan that otherwise would have delivered what the client was looking to get. And it could have only happened to this degree at Pacific Life.

For that reason, it strikes at the heart of what Pacific Life has been doing with adjustable compensation for decades. It is a massive threat. You can imagine a scenario where every 100% Basic Coverage policy gets looped into a class-action lawsuit. But what about 90% Basic? Or 80% Basic? Or 20% Basic? That’s where this case gets dangerous. It cracks open a whole slew of issues about how agents get paid and how commissions are recaptured in policy charges for all life insurers, not just Pacific Life. There has always been talk of a case that would challenge the underpinnings of commissions in this industry. It was only a matter of time. This may very well be the one.

It is pure coincidence that I wrote #442 | A New Era for Blending at Pacific Life a couple of weeks ago and happened to publish it the same day that Kyle and Samantha made their announcement. The crux of the article is that Pacific Life has finally started to provide a different blending structure for agents, starting with the recently-released Venture 2 UL. Commission-free ART Coverage is gone. The product now offers Basic Coverage and Long-Term Performance (LTP) Coverage. LTP does offer lower Target premiums, but is still in line with the rest of the industry, and brings along a suite of new performance tradeoffs. Basic Coverage allows for above-market compensation, but only just so. The new blending structure in Venture 2 UL is reportedly going to make its way to all of Pacific Life’s products. The change might be seen as a tacit acknowledgment that the old way of blending had issues. PacLife seems ready to move on. The question is whether this case will let them.