#435 | The Securitization Frontier

A Primer on Securitization

Securitization is one of those words that means nothing to the vast majority of humans and yet, unbeknownst to them, their financial lives intersect with securitization on a regular basis. If you have a mortgage, chances are very good that mortgage has been bundled with other mortgages in a residential mortgage-backed security. Every time you step foot in a store, hotel, office building or restaurant, you might be entering a building that was purchased with a commercial mortgage that is now in a commercial mortgage-backed security. Have a car payment? Credit card payment? Cell phone plan? Any installment plan? Your payments might be going to an asset-backed security. Work for a small business funded with debt? That debt might be owned by a collateralized loan obligation.

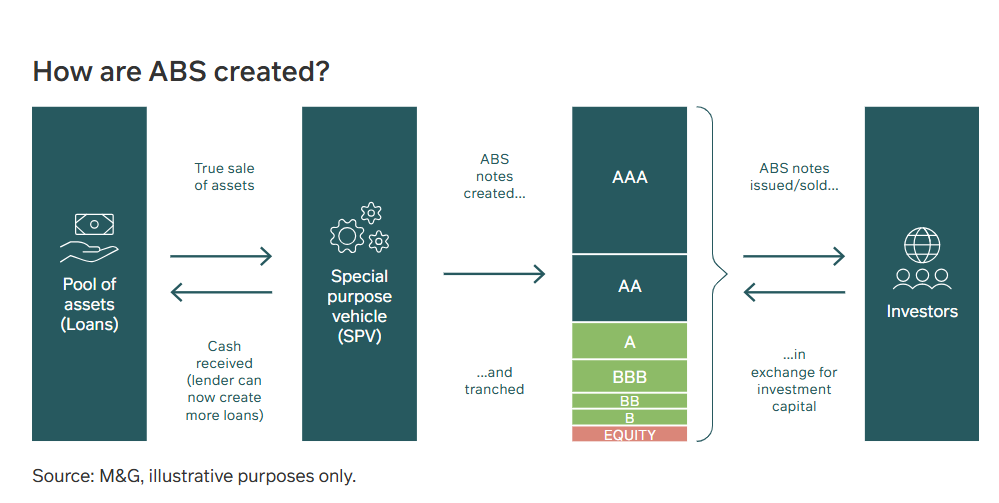

The core concept behind securitization is in the name itself – the bundling of individual assets producing cash flows into an investible security that can be valued and traded. In its simplest form, the new security would be just a pro-rata share of the income, gains and losses of the underlying investments. It would probably be structured as a mutual fund, unit investment trust, real estate investment trust or an ETF. The benefit to investors is simplicity, diversification, liquidity and the expertise of the manager selecting the assets. It’s a huge improvement compared to a world where individual investors can only purchase individual assets.

Securitization, however, goes a step further. Rather than just offering pro-rata shares, securitization restructures the exposures in order to create different investment profiles for each distinct investment tier, called tranches. The aggregate risk and return remain the same, but the risk and return for each tranche is different. One pool of mid-grade auto loans, for example, can be transformed into tranches ranging from sparkling clean AAA-rated debt all the way to near-radioactive speculative equity.

The transformation process is a matter of prioritization. The AAA-rated tranche is first in line for cash flows from the underlying assets and last in line for losses. The equity tranche is the inverse – last in line for cash flows, first in line for losses. In between are usually a range of tranches that fall behind AAA and above the equity position, usually (in order) double-A, single-A, triple-B and double-B. Each one offers a distinct risk/return profile that is can be easily compared to traditional corporate bonds with the same rating. A generic Asset Backed Security (ABS) structure looks like the flow chart below.

From one vantage point, securitization allows for industrial-grade manufacturing of marketable rated fixed income assets to be purchased by institutional investors that need that sort of thing – banks, mutual funds, pensions and, you guessed it, life insurers. Only so many companies are issuing bonds, but our entire economy is swimming in consumer, real estate and middle-market business debt. All of that stuff can be scooped up, securitized and consumed by institutional investors as rated fixed income assets. It’s a magical system.

Every article that I write sort of takes a life of its own and this article is pulling hard toward the big storyline about life insurers buying boatloads of securitized fixed income assets manufactured by alternative asset managers like Apollo, Carlyle, Blackstone, Ares and others. That’s not where I’m going this time, though, because I’ve already covered it in #431 | The New Risk Free Rate and several articles prior to that, including #383, #358, #355, #345, #289 and even as far back as #136.This time, we’re going somewhere else entirely – what happens if the asset being securitized is a life insurance policy?

Historically, life insurance securitizations have revolved around use cases for both investors and insurers. Life settlements are the classic example. Rather than investing in each individual policy, securitization allows investors to have access to a pool of settled policies that require on going premiums and pay death benefits. However, the complexities and timing of assembling the policy portfolio has made settlement securitizations relatively rare. During the heyday of Guaranteed UL, some life insurers turned to securitization as a way to finance “redundant” reserves, allowing a cheap and product-specific source of capital. As the securitization machine continues to crank, life insurance cash flows will undoubtedly find their way into the maw to be consumed by institutional investors, including life insurers themselves, with effectively no direct downstream effects to agents, brokers and policyholders.

The more interesting question, however, is what would happen if securitization was used for the benefit not of investors or insurers but the policyholder. Imagine a scenario where, for example, a policyholder could assign their policy to a pool of hundreds of similar policies and receive, in return, a fractional interest in the pool. They would give up the specificity of the death benefit payout for planning purposes, but they would receive a level of risk diversification and cash flow consistency that is unattainable for an individual. This sort of structure would, for lack of a better term, institutionalize life insurance ownership. Whether or not a client chooses to hold the policy outright or to securitize it is a matter of choice – do they want a single, large payout at an unknown time or would they rather have many, smaller payouts at relatively predictable times?

In order to make this sort of policy securitization work, you need lots of policies that are similarly structured with relatively similar demographic profiles that are owned by people with a universally shared preference for predictable cash flow over single-event mortality payouts. You need, in other words, some sort of institutional life insurance ownership to really make it work. COLI and BOLI obviously fit, but so does a little-known corner of the industry – life insurance used by credit unions.

Credit Union Split Dollar

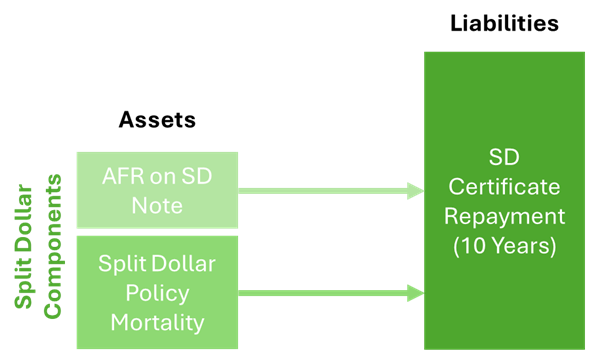

The standard structure for these transactions is (typically) loan-regime split-dollar. The credit union pays the premiums for the benefit of an executive. At the death of the executive, the credit union is repaid premium plus accrued interest typically at the long-term AFR. The benefit to the executive is the ability to use the cash value for tax-free retirement distributions, as long as there is enough residual value to eventually repay the credit union. If all goes well, there may also be residual death benefit that goes to the executive’s family, but the primary purpose of the transaction is to create a supplemental retirement plan for the executive. The cash flows for the transaction look like this:

Any leveraged transaction – and split-dollar is certainly leveraged – is inherently fragile. The only certain part is the fact that the credit union pays premiums on behalf of the executive. Full repayment to the credit union is contingent on the rate of return on the death benefit exceeding the long-term AFR. Right now, long-term AFR is nearly 5%. That’s a pretty high bar to clear. But most of these policies were put into place when long-term AFRs were low. In 2020, the long-term AFR was hovering just above 1%. That’s a terrible thing for the credit unions, which effectively have a dead asset sitting on their balance sheets for an unknown period of time in the form of a split dollar receivable, but a spectacular thing for the executives themselves.

Performance in excess of what is required to repay the split dollar note to the credit union is eligible for distribution to the executive in the form of tax-free retirement income and residual death benefit. Practically, actually getting the distributions out of the policy is much more complex. It requires a delicate dance between maintaining sufficient death benefit to repay the split dollar note and giving the executive the income that they expect from the policy, regardless of whether their expectation is reasonable.

One of the reasons why Indexed UL has been such a prevalent part of the market for split dollar in credit unions is that the delicate dance isn’t really that delicate if you can assume an 8% illustrated rate. There’s more than enough margin to pay back the credit union and to deliver substantial income to the executive. The problem, of course, is that the real world is not an illustrated rate. Indexed UL caps are continuously changing – painfully so for the thousands of Securian policies used in CU-backed split dollar plans that are sitting in the old portfolio with 7.5% caps. Little wonder why the firm that sold them doesn’t even show updated in-force illustrations to the credit unions. Ignorance is bliss.

Split dollar is inherently a compromise. The credit union ties up capital at sub-optimal rates for an unknown period of time in order to fund an uncertain benefit to the executive. What both the credit union and the executive want is certainty. Illustrating conservatively and using two policies to support the transaction rather than one both serve to enhance the level of certainty of outcome, but both fall short of an explicit guarantee. If you want that, then you have to think outside of the normal life insurance structure. You have to think about securitization.

The LifeNotes Alternative

Enter LifeNotes, a securitization structure designed specifically for the credit union space. At the heart of LifeNotes is a very simple observation – credit unions funding split dollar programs want their money back as soon as possible and are willing to give up earning interest to get it. This makes perfect sense. Capital that has been tied up in split dollar programs is the worst asset on the credit union’s balance sheet. It earns virtually nothing and is tied up for an indefinite period of time, potentially decades. It’s the perpetual callable bond from hell.

LifeNotes offers credit unions the ability to effectively “pay” their AFR interest to get a guaranteed repayment after a designated period of time. The mechanics are simple. The credit union assigns the split dollar note to LifeNotes in exchange for a certificate that is payable at par at the designated future date – in 10 years, for example. LifeNotes, then, has to figure out how to convert the AFR interest into enough cash flow to make sure that there is money to repay the certificates.

This is no small feat. AFR interest compounding at 2% over 10 years is around 22%. Most executives in these mature plans are in their mid-50s,let’s just say 55. Cumulative mortality over the 10 years from age 55 to age 65 is about 6%. Assuming that the death benefit is twice the cash value, which is close to CVAT corridor, then the payout relative to the size of the outstanding split dollar loan is about 12%. That gives us a total of 34%, far less than the 100% needed to satisfy the certificate. The cash flows look something like this:

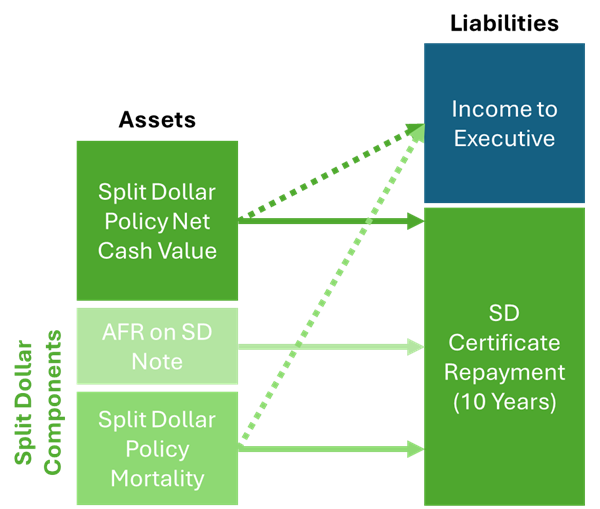

The obvious solution is to use the cash value from the policy to repay the certificate, but there is a huge problem with that approach – the executive owns the policy, not the credit union. In order for LifeNotes to have access to the cash value, it has to incentivize the executive to collaterally assign all of the policy benefits, but not the actual ownership, to the LifeNotes trust. This is not a life settlement or STOLI transaction where the executive receives cash in exchange for ownership transfer. LifeNotes isn’t about policy transfer – it’s about policy transformation in a way that is only feasible with securitization.

Herein lies the second great insight that is key to LifeNotes. The Executive is often willing to trade their upside in the form of potential future policy performance and a retained death benefit in exchange for guaranteed income, particularly if the plan is underperforming, hasn’t been optimized by one of the experts in this space or if the Executive doesn’t really understand the upside potential. LifeNotes gives them the option to have guaranteed income in exchange for purchasing the full economics of the policy. In doing so, LifeNotes can put the full death benefit to work to help satisfy the repayment obligation to the credit union. But it also now can borrow against the cash value to repay the obligations, so long as it either allocates a certain amount to pay the guaranteed income or purchases a separate annuity.

Now we have a structure that looks like this, with solid lines denoting first use of the cash flows and dotted lines denoting second use:

The introduction of cash value bridges the duration gap. The income obligation to the executive is long – far longer than the repayment of the split dollar certificate. Cash value that is used to satisfy the split dollar certificate will be replenished over time by death benefit payouts that can also go to support the guaranteed income amounts. LifeNotes manages the delicate dance required by any split dollar transaction and, at the same time, gives everyone exactly what they want in terms of payoff.

Because the Executive is giving up their share of the death benefit, LifeNotes can offer an income guarantee that is comparable or even slightly higher than what is shown on the in-force policy illustration – for a Whole Life policy. For Indexed UL, the income guarantees are much lower. This is completely counter to the prevailing narrative that Indexed UL will outperform Whole Life for income based on illustrated returns. But as I’ve written many times, illustrated income using the maximum AG 49 rate is a sub-50% success proposition.

That’s unacceptable for LifeNotes because they have to guarantee the income. They care more about certainty than upside. As a result, they have to bid the income guarantee on an IUL at a substantial discount to the illustrated income. It’s no surprise, then, that the vast majority of the policies in LifeNotes are Whole Life, not Indexed UL. Executives don’t seem to want to believe that their illustrated income from Indexed UL is anything but rock solid – despite a fair market, third-party valuation from LifeNotes that shows a discount.

In the simple model we’ve built so far for LifeNotes, the challenge is that everything has to work perfectly with very little margin for error. Mortality has to come in exactly as planned. Policy performance has to be sufficient to be able to cover the guaranteed income and the repayment obligations. There is not a lot of liquidity backstop if either of those things goes awry. And, on top of that, there’s no room to pay any fees to the folks who created the structure because it’s a self-enclosed loop. For all of those reasons, this is actually not how LifeNotes works, at least not in its entirety.

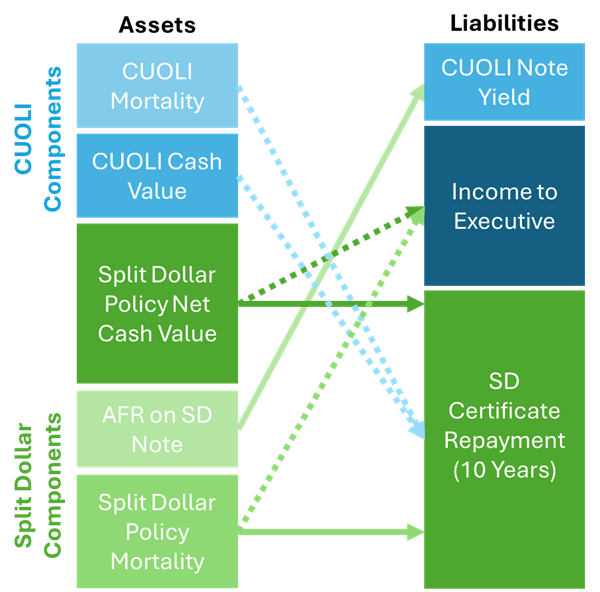

Herein lies the third key observation – the AFR interest on the note can be put to better use than simply satisfying a liquidity call. If the credit union is willing to give up interest, then why not pay that interest to someone else who can satisfy the liquidity demands? In other words, why not use AFR to “buy” liquidity from someone else? And what if that liquidity also came in the form of life insurance assets with their own death benefits coming along for the ride that can be used, over time, to replenish the structure?

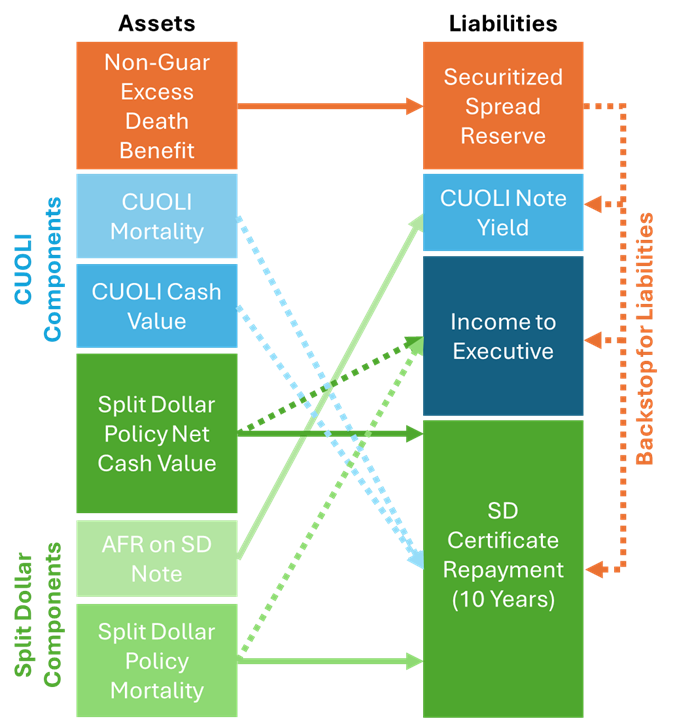

Credit Union Owned Life Insurance (CUOLI) offers exactly that opportunity. Unlike the split dollar plans, the credit unions hold CUOLI directly on their balance sheet as a high-quality, tax-free asset class a la BOLI and COLI. Credit unions can assign their CUOLI to LifeNotes in exchange for a note yielding SOFR plus 270bps (current pricing) with a specific maturity date, which is funded by redirecting the AFR interest from the split dollar notes to the CUOLI notes. This gives the credit unions what they want – a higher yield – and LifeNotes the liquid assets and death benefit payouts that they need to satisfy their split dollar certificate obligations. LifeNotes manages the ratio of split dollar notes to CUOLI assets so that there is enough AFR interest from the split dollar notes to meet the obligations on the CUOLI side. Now the structure looks like this:

The addition of CUOLI creates enough liquidity that, along with natural mortality payouts and the assigned cash value of the split dollar policy, it is a virtual certainty that the split dollar certificates will be fully satisfied. Think of that as the bulletproof, AAA-rated tranche of LifeNotes. If LifeNotes can’t fulfill that obligation, then it can’t exist. All of the liquidity pouring into the trust structure is designed to first pay back the split dollar obligations, then to satisfy the income needs of the executive and, finally, to deliver on the yield promises made to the credit unions who contributed CUOLI. It’s a classic securitization stack, with one thing missing – equity.

Here’s where things get interesting. LifeNotes is carefully balanced to ensure that inflows meet outflows on a guaranteed basis. The life insurers are all highly rated, which virtually eliminates the possibility of a default. The split dollar and CUOLI policies are assumed to perform only at the guarantees for the purposes of calculating current value to feed the income to the executive and liquidity for future trust obligations. LifeNotes is calibrated to survive the worst case which, again, is one of the features of all securitized structures. But if the worst case doesn’t come to pass and things actually turn out better than expected, then the benefits accrue to the equity sleeve of the securitization structure.

In LifeNotes, the equity position is referred to as Securitized Spread. There are two ways that it accrues to the trust. The first is through non-guaranteed policy performance, which materializes in the cash flows as additional death benefit amounts over time because all of the policies are held to maturity. The credit unions contributing split dollar notes don’t receive Securitized Spread because they didn’t contribute any death benefit – but neither does the Executive because they traded it away in exchange for guaranteed income. Credit unions contributing CUOLI, however, do have a stake in Securitized Spread.

The other source of Securitized Spread is investment management. In the diagram so far, there’s no room for investment management. But in practice, this is a huge piece of what makes LifeNotes work. As I’ve argued in many articles, life insurance cash value is an asset whether people think of it that way or not. For LifeNotes, it is definitely an asset – a highly liquid, easily collateralized asset. One option is to just let it sit in the policy and continue to grow. For healthy contracts with strong returns, that makes sense.

But another option is to borrow it out with a policy loan to buy more attractive assets. Credit unions have regulatory constraints on what they can own and LifeNotes shares those same constraints for investments that use cash value as collateral. A natural investment is to buy better life insurance policies on the secondary market because, like CUOLI, those have both cash value and death benefit payouts. They can also invest in highly rated bonds and certain real estate structures. Nothing crazy – but in an inverted yield curve environment, it might make sense to leverage dead life insurance cash values to get something more interesting.

Both strong policy performance and attractive investment returns first contribute to a further liquidity backstop for covering the guaranteed outflows coming out of the trust. To the extent they are more than what’s required, they accrue in a Securitized Spread reserve. If the trust has issues in the future, the Securitized Spread can be used as a reserve to make note-holders whole. But if things go to plan, the Securitized Spread reserve will eventually be paid to who owns it. Some goes to credit unions as an incentive for them to contribute their CUOLI, but the bulk of it goes to LifeNotes as an incentives to manage the structure well and deliver the goods. Here’s how the cash flow works with Securitized Spread:

Unlike the underlying trust investments, Securitized Spread can be invested freely. Some of the negative noise around LifeNotes is the claim that the core trust benefits are being funded in part by speculative investments. That’s not true. The core benefits of LifeNotes are being funded through assets that have to fit in the standard box for credit unions. Only the excess gains accrued in the Securitized Spread can be invested more exotically. The incentive for LifeNotes is to manage those assets both for yield and for security because, ultimately, LifeNotes is the one who profits the most from strong investment performance. The incentives are properly aligned.

The simple story for LifeNotes is that it gives everyone exactly what they want. Credit unions with split dollar notes get paid back, even though they’re giving up AFR interest. Executives get guaranteed retirement income by giving up residual death benefit and upside potential in policy performance. Credit unions with CUOLI can trade a low-yield asset for a higher yielding note, plus the potential to get a piece of Securitized Spread. And, of course, LifeNotes gets to orchestrate all of this in exchange for potentially millions in fees. This is classic securitization. It’s all about bundling assets to create more desirable tradeoffs than what is available in any individual asset.

The full story is, as you can imagine, substantially more complex. I signed an NDA with LifeNotes to get full access. I’ve spent many hours digging through their materials, all the way down to the note documents and trust agreements, and more than a few hours peppering their leadership team with questions. There are several LLCs involved that play different roles. The cash flows aren’t quite as clean as what I showed above. There’s a lot of technology in the background designed to execute the strategy. It’s really hard, if you were just to look at the core documents, to see the forest for the trees.

That’s always the case with securitization. Look closely and it seems almost unfathomably complex. Pull back a little bit and the story is pretty simple. That’s true for any securitized structure and it’s true for LifeNotes, too. The challenge for anyone investing in a securitized structure is reconciling the fact that they’ll probably never fully understand all of the intricate dynamics but still having confidence that it’s going to do what it’s supposed to do. In mortgages, government agencies step in to bridge the gap with implicit federal guarantees. In structured credit, specialty managers and big banks with long track records rely on their experience and reputations. You can’t access the benefits of securitization without some level of trust – and maybe even a little bit of faith.

The real challenge of LifeNotes is simply that it’s new, untested and effectively unbranded. I’ve dug through their core documents and it is obvious that there have been a lot of third-party eyes on this structure. The offering memorandum is as comprehensive as any securities filing I’ve seen from a life insurer. They have third-party audits, including one from Doeren Mayhew, the predominate auditing firm for credit unions. From what I can tell, it’s designed to do exactly everything that it says it will do. But ultimately, it’s very difficult – maybe even impossible – to know for sure. Is it possible that LifeNotes can’t fulfill its obligations? Of course. If insurers go bust and people suddenly stop dying, there won’t be enough cash to go around. But that risk would exist regardless of LifeNotes. What matters is the incremental risk – the risk that LifeNotes is miscalibrated and writes checks that it can’t cash.

If the structure had Goldman Sachs’ name on it, no one would think twice about it. But LifeNotes isn’t Goldman Sachs. Credit unions working with LifeNotes are trading individual insured, policy and insurer risk for counterparty risk in the LifeNotes structure. That’s a huge deal. Counterparty risk is one of the key risk factors that bank and credit union regulators try to manage. Right now, the credit union regulator hasn’t specifically opined on the LifeNotes structure. And as a result, it’s incumbent on any credit union to do due diligence on the structure and the team to make sure they’re comfortable with the counterparty risk. The less due diligence you do, the more you rely on trust and faith. A better strategy is, as the saying goes, to trust – but verify. And in my experience, LifeNotes is more than happy to support the verification process.

Securitization and the Future of Life Insurance

The mere existence and early success of LifeNotes, which is about to close out its first $500 million fund, opens up a whole bunch of questions about how securitization concepts might be applied more broadly for the benefit of individual policyholders. I would argue that one of the reasons LifeNotes is the only firm trying to do life insurance securitization is because life insurance is – despite its pedestrian reputation – a highly complex and multi-faceted financial instrument. In order to securitize life insurance, you have to deeply understand both securitization and life insurance. There are, maybe, a couple of people in all of humanity who understand both – and I’m not one of them.

A fitting analogy of a pedestrian product with surprisingly tricky dynamics is a vanilla fixed-rate mortgage. Investing in mortgages is notoriously complex because of convexity, the phenomenon where mortgages get refinanced as interest rates drop, which shortens the duration of the portfolio and causes the price of the mortgage bonds to change in ways that are completely different than normal fixed-rate bonds. Buying any mortgage portfolio to match a liability requires a deep understanding of convexity dynamics. Sounds pretty complex, right?

That is child’s play compared to life insurance, which can be broken into a wide range of constituent cash flows and allows for an enormous amount of policyholder flexibility that materially impacts how cash flows emerge over time. Reinsurers, in many ways, fill the typical role of securitization in the insurance space. They’re experts in underlying risk and will take specific risks on a YRT basis and bundles of risk through a range of coinsurance structures. The sheer complexity of life insurance liabilities has historically meant that only the experts – the reinsurers – can take one-off risk bets. But we’ve seen securitization fill the gaps elsewhere, most notably with CAT bonds in the P&C space, where investors buy bonds specifically designed to cover event-driven risk and receive huge yields if the risk doesn’t come to pass. It’s reinsurance, democratized.

It’s possible that securitization of life insurance liabilities becomes as common as CAT bonds, but I don’t think so. The market isn’t big enough and the knowledge barriers are too high. The more interesting angle, I think, is securitization in a way that is designed for the policyholder. A really simple version might look like a structure where the original policyholder contributes their policy to the trust in exchange for participating in the index while farming out the NAR to another noteholder who pays their COIs but receives the NAR at death. Both parties would get exactly what they want. The policyholder gets tax-free cash value growth and the other noteholder gets a mortality-linked payout. It’s effectively a split-dollar plan, but without the typical business and estate planning angles.

On a grand scale, arrangements like this could overcome typical insurability issues for people who want to use life insurance for accumulation and allow others to monetize their insurability while still retaining what they need for death benefit protection by maintaining a minimum level of NAR. This prospect is, I think, simultaneously exciting and terrifying. It’s exciting to think about the idea of broadening the appeal of life insurance by creating more customized structures through securitization. That is very cool. It’s the institutionalization, if you will, of life insurance.

That’s exactly why the prospect is also terrifying. More than we’d like to admit, the life insurance complex relies on flying under the radar. The obvious example is the generous level of tax control provided to policyholders that is often misconstrued as a pure “tax advantage” and abused in structures that are egregiously focused on shielding asset growth from taxes, particularly in PPLI. Also obvious is the profusion of insurance agents casting themselves as financial advisors and sell life insurance as investment vehicles even though they don’t have a securities license or even a Series 65. Less obvious, but no less problematic, is the fact that many life insurance policies are priced on the presumption of sub-optimal policyholder behavior in order to support carrier profitability.

Attention is weight. Gather too much of it and pieces of the entire life insurance structure start to crack. Securitization structures highlight the particular use-cases of life insurance, particularly its tax and cash flow benefits that currently remain safely ensconced inside the protective bubble of the death benefit. Securitization could separate the two into its constituent pieces, which would expose the cash flow benefits to further scrutiny. There are offshore structures that already do this sort of thing in the private placement market by using other lives to supply the insurance. Securitization merely takes the concept further.

Exciting or terrifying, one thing seems certain – LifeNotes is the first but almost certainly not the last securitization structure that we’ll see in the industry. Life insurance and annuities generate a lot of cash flow that has garnered a lot of attention from investment managers that specialize in securitized investments. It’s only a matter of time before these firms start to gather up life insurance and annuity policies into their own securitized structures for the benefit of investors, yes, but also insurers and policyholders themselves. Securitization isn’t bad or good, evil or benevolent. It just creates new tradeoffs for what already exists – and it’s hard to imagine that, in the long run, that won’t be beneficial to the industry and its participants.