#421 | Risk and Reward in Protection Sales

Just 20 years ago, the hottest ticket in life insurance was middle-market estate planning. The estate tax exemption was just $2 million – low enough to ensnare more than two million households with a net worth in excess of $4 million. At the same time, cheap Guaranteed UL was flooding the market, offering a low-cost alternative to traditional Whole Life. Selling life insurance is never easy, but it was about as easy as it could have been back in those heady days.

As the estate tax exemption rose, sales of Guaranteed UL and all other protection-oriented life insurance policies fell. Consider the fact that Guaranteed UL made up more than 50% of all permanent life insurance sales in 2007 and at the end of 2023 it made up just 1.5%. The mantel of lifetime guaranteed universal life has instead been taken up by Indexed UL and Variable UL, but both of those variants together add up to just 5% of the overall life market by premium. The market has made a pronounced shift over the past decade away from secondary guarantees and towards accumulation-oriented products, which now constitute the vast majority of new sales in permanent insurance products.

This shift has left the life insurance market somewhat underdeveloped at a critical juncture. The current estate tax exemption of $13.61M per individual is scheduled to drop to $7M in 2026. Theoretically, that opens up at least some families to an estate tax liability that could be solved by life insurance. But even more importantly, rising rates have clamped down on the appeal of fixed insurance products for accumulation. Whole Life sales are down 6% so far this year. Indexed UL, which has temporarily benefited in terms of illustrated performance by switching to new portfolios, is up just 1%. Variable UL, by contrast, is up 17% through Q3 and is being driven by large-face, accumulation-oriented products. The time seems ripe for a resurgence of protection-oriented products.

We’re already seeing the first few signs that it’s happening. Pacific Life is emerging as a dark horse in the single-life lifetime secondary guarantee space. Nationwide and Securian have launched new Survivorship VUL offerings with secondary guarantees. AuguStar and Symetra have rolled out new protection-oriented Indexed UL offerings with limited guarantees. Principal extended the secondary guarantee period to age 100 on Provider Edge II. There’s quite a bit of new product activity in this little corner of the market.

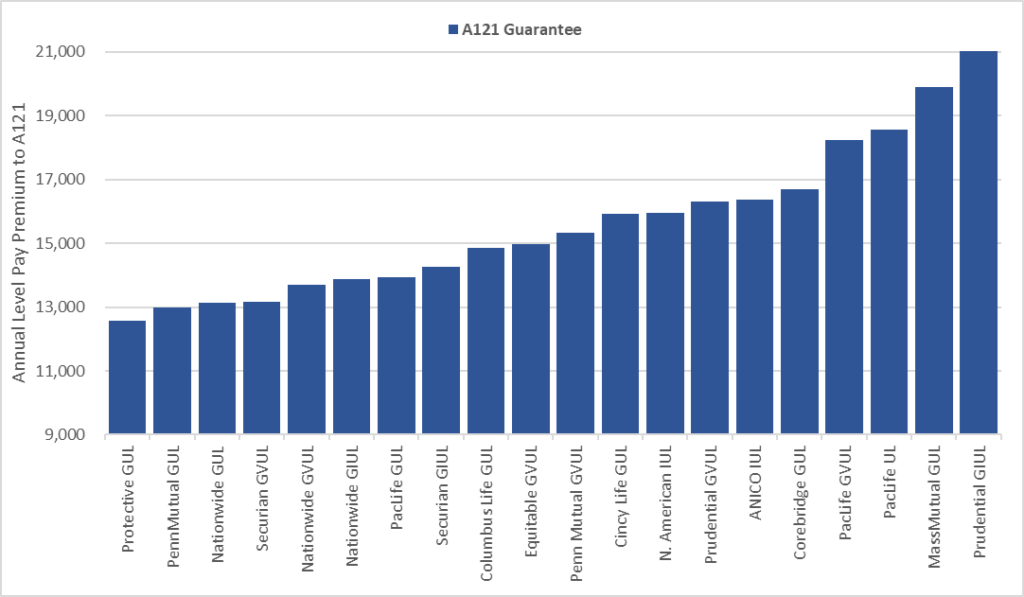

The challenge is knowing what to do with all of these new products and protection-oriented products in general. Producers working in this space have historically relied on pricing for secondary guarantees for recommendations to their clients. Although secondary guarantee inventory has declined, it hasn’t disappeared. Below is the level pay pricing for an age 121 secondary guarantee on a 55 year old Preferred Male for $1 million of death benefit for 20 products offered by 13 major insurers:

I’ve been tracking this particular pricing cell for over 15 years. Back in the heyday of Guaranteed UL, it wasn’t uncommon to find carriers flirting with the $12,000 mark for lifetime guarantee pricing. Someone always seemed willing to step up and bite the cheese. Currently, it’s Protective, with a quoted price of $12,564 for Lifetime Assurance UL. Right behind Protective with sub-$14k pricing are Penn Mutual, Nationwide, Securian and Pacific Life, followed by Columbus Life at just under $15k.

Is it a coincidence that all five of those firms are mutual companies and Protective is a Japanese subsidiary? I don’t think it is. There is a case to be made, in today’s economic environment, that Guaranteed UL could prove to be profitable if interest rates stay elevated. Domestic stock companies have learned the hard way that Guaranteed UL is radioactive for investors regardless of the company’s models and expectations. Just ask Lincoln, Prudential, John Hancock and Brighthouse. Mutual companies and international firms, however, have the latitude to take the bet. Whether or not they should is a separate question.

Regardless, the fact that some mutuals are taking the bet on secondary guarantees is a problem for the mutuals that aren’t. I’ve seen an avalanche of proposed exchanges recently from in-force participating Whole Life contracts to UL policies with secondary guarantees and, for whatever reason, particularly Pacific Life’s Admiral VUL. The pitch is pretty simple – the client receives a higher death benefit immediately and the potential for long-term upside performance from strong subaccount performance. What’s not to love? Take a look at the graph below showing death benefits for a hypothetical in-force Whole Life policy issued on a 45 year old being exchanged to a brand new Admiral VUL policy (with the same underwriting class) at attained age 55, age 65 and age 75 and illustrated at 6%.

It is certainly true that the client receives a higher death benefit in all three scenarios. It’s also true that in two of the scenarios, the age 55 exchange and the age 65 exchange, long-term cash value performance pushed up the death benefit. But what is also true is that the Whole Life policy delivers more death benefit for all three scenarios in the heart of the mortality curve. In other words, Whole Life has a higher death benefit when it counts more – and that’s based the current dividend rate, not a hypothetical subaccount return assumption. Making the exchange is a lot riskier than it looks.

The problem with this exchange scenario and any exchange scenario, in general, is that buying a new policy entails new acquisition expenses. In the case of the 55 year old, new acquisition expenses related solely to the cost of making the exchange eat up 54% of the 1035 amount. For age 65 and 75, the figure is closer to 35%. Think of it in simple terms – the new company has to deliver more benefits with less money than the old company. How is that possible? Often, it’s not. But in the case of these sorts of exchanges, the argument is that initial death benefit is more benefit even though, in reality, later death benefit is what counts. The only way that the new guaranteed VUL, in this case, delivers the goods later on is with spectacular subaccount performance. That may be reason enough to make the exchange, but it’s a risky bet.

In most situations, the proposed exchange is to move from a safe product to one with more risk and, potentially, more reward. In this example, the reward is better short-term death benefit but with the risk of worse long-term death benefit. Is that an appropriate exchange? That’s hard to say. As an industry, we do a terrible job of framing life insurance in the context of risk. We’re great at pointing to numbers that show up 30 years into the future on illustrations that explicitly say they are not reliable projections and have a 0% likelihood of coming to pass. We are not so good at actually having real discussions about risk and reward.

The same risk/reward dynamic shows up for products that purport to be protection-oriented but don’t have long-term guarantees. Whole Life represents the going rate for full risk transfer with an experience refund in the form of a dividend. Penn Mutual offers Protection Whole Life with an annual premium of $23,000 for the cell that I’ve been using for this analysis. That’s about as cheap as it gets for Whole Life and many other mutuals would contend that, even then, Penn Mutual is taking some level of pricing risk with that product. MassMutual’s Whole Life premium for the same cell is $31,180.

But no matter what way you cut it, those figures are vastly higher than what we see in market for secondary guarantee products. Who takes the risk in that scenario? The carrier. Despite Pacific Life’s sterling ratings and demonstrable financial strength, the simple fact that they are writing risky policies means that they are a riskier proposition than a company that won’t write those types of policies at that price. More risky policies mean more risk for the insurer. At one end of the spectrum is Northwestern Mutual, which essentially takes no financial risk and shares profits through participating dividends. At the other end of the spectrum is PHL Variable. Every other life insurer exists somewhere along that continuum, at least in terms of retained product risk.

But what about the plethora of products without lifetime guarantees that offer even lower illustrated premiums? Take a look at how those products stack up when illustrated at their maximum rates for UL/IUL and at 10% gross for VUL:

It should come as no surprise that the most expensive product on the list is a Guaranteed UL issued by a true-blue mutual insurer and the cheapest product is a Variable UL illustrated at 10%. That makes sense. But the finer comparisons are much more difficult. Which one is riskier – John Hancock Protection VUL illustrated at 10% with a $9,506 premium or Protection IUL illustrated at the maximum AG 49 rate with an $11,061 premium? It feels like the answer is obviously the VUL. It has the higher illustrated rate and the lower premium. Surely, it has to be riskier?

Not so fast. A VUL policy invested in straight equities is a different animal than an Indexed UL policy with merely index-linked credits. The illustration regime for Indexed UL uses look-back performance assuming a constant S&P 500 Cap. A 10% Cap yields an illustrated rate of 6.29% based on historical performance of the S&P 500 price index. If you take the same exact methodology and apply it purely to the S&P 500 with reinvested dividends, than you get a little over 11%. In other words, the risk of an 11% illustrated rate in a VUL is roughly equivalent to the risk of an Indexed UL with a 10% Cap illustrated at 6%. I did this analysis a few years ago with actual stochastic (variable) index returns and the results are below

This raises a secondary question – what’s the appropriate rate for illustrating these two products? Illustrating at the standard AG 49 rate for IUL or 11% for VUL results in a lapse probability greater than 50%. In other words, these products demonstrate low premiums because the client bears an enormous amount of performance risk. Missing the bogey results in a lapse.

One of the truisms for life insurance is that the cure has to be better than the disease. The entire point of life insurance is risk transfer. But if you set up a policy from the outset with a huge performance hurdle that it has to clear, then risk is being retained, not transferred. My experience is that agents essentially never talk about life insurance in these terms. It’s much easier to tell the client that cheaper is better. In reality, cheaper isn’t better – it’s just riskier.

Retained risk in life insurance is really hard to conceptualize because it combines short-term volatility, long-term variability and non-linear policy charges all in one thing. Everyone is familiar with short-term volatility. Long-term variability is the actual deviation of performance from the long-term average. Easy enough. But then layer on non-linear policy charges that operate independently of the assets and you get something much, much trickier.

Consider, for example, the simple chart below. The black line is the illustrated performance of a policy funded to endow at maturity at a certain illustrated rate. It’s a nice, smooth curve that does exactly what it’s supposed to do. It’s what essentially every illustration shows. The premium is around $10,000 per year. Now, what happens if the client pays $1 more or $1 less each year? The policy lapses prematurely or it shoots to the moon – for a $1 variance. The same is true for something like a 10bps difference in level return assumption. And, of course, sequence of returns can have the same effect. Very, very minor changes reverberate over the course of the policy into enormous differences in outcomes

That’s for a $1 premium change. The other lines show more impactful changes. Consider that with just a $100 change, less than 1% of the premium, the policy lapses at age 100 versus age 121 or it over-endows. With a $1,000 change in premium, it has cash value in excess of the death benefit as early as age 80 – or it lapses at 92. These are enormous differences for relatively slight variances that can manifest either as simple premium differences or long-term return variance or short-term volatility. Non-linear charges turn molehills into mountains.

Given that is how life insurance works, then it would follow that setting the premium for a life insurance policy needs to take this non-linearity into account. All illustrations should have a buffer. Unfortunately, buffers aren’t sexy. Agents like to show the cheapest premium, not the one that is most likely to work over the long run. If we take the same benchmark of products and run the VUL policies at 6% and the IUL/UL policies at 4.5%, both of which seem like very reasonable long-term performance assumptions and roughly equate the inherent risk of the two products, then we get very different premiums across the industry. Take a look at the chart below.

Gone are the sub-$10k premiums. The outliers in this analysis are John Hancock Protection UL and Principal UL Provider Edge II. Both policies have the benefit of flat COIs* – in other words, linear charges, not non-linear charges. As a result, the change to the interest rate is less impactful for those two products. But designing a policy with flat COIs is risky unto itself, which is why John Hancock delivers flat(ish) charges in Protection UL through a complex interaction of actual COIs and the Policy Value Credit, as detailed in other articles, that ultimately pushes the risk back onto the policyholder.

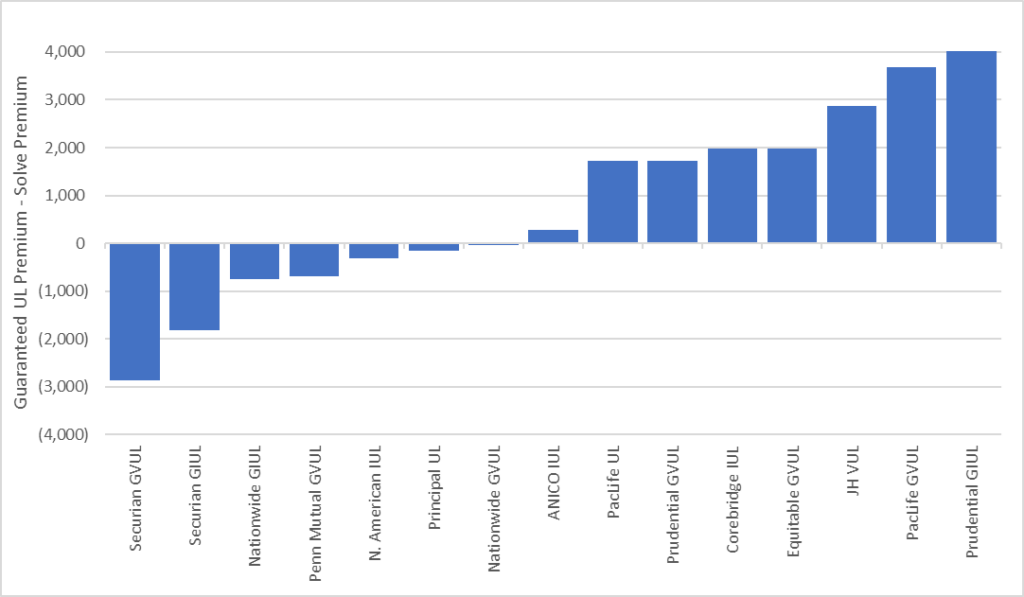

Many policies also offer the option to add a guarantee to a policy for a cost. See below for the marginal cost of adding guarantees to age 100 or beyond relative to the premium when solved at the conservative 6% rate for VUL or 4.5% for IUL/UL:

Products with a negative cost to adding the long-term guarantee imply that the carrier is embedding a higher earned rate assumption for the purposes of determining the cost of the guarantee than the 6% or 4.5% rate assumption. On the other side of the chart, the carrier is being more conservative than the 6% or 4.5% rate assumption for setting the guaranteed premium. Ultimately, it all comes down to risk. Some carriers are willing to take the performance risk onto their own balance sheets. Others aren’t. And if the carrier isn’t taking the risk, then guess who is? The policyholder.

This brings us back around to the fundamental question of how producers and their clients should approach the challenge of retained risk in life insurance policies, particularly protection-oriented policies where the downside is lapse. The approach that the industry has traditionally used is to simply ignore the question and pretend that the cheapest policy is the best one. That didn’t work for UL in the 1980s, nor VUL in the 1990s, nor GUL in the mid-2000s and it won’t work for IUL, either. Permanent insurance is a financial product with a complex and distinct risk/return profile. It should be understood that way by all of the parties in the transaction.

Fortunately, there’s a simple fix. Unfortunately, almost no one is going to like it. The goal of a protection-oriented sale is not, under any circumstance, to sell the cheapest product. If you sell a cheap Guaranteed UL, you’re banking that the insurer isn’t selling so much cheap GUL that they blow themselves up. If you sell a cheap Indexed UL, you’re banking that you get extremely strong index performance, have a favorable sequence of return profile and that the carrier doesn’t change the product rates for the next 50 years. If you sell a cheap Variable UL, you’re banking on volatile and variable separate account performance consistently working in your favor. Cheapness always means riskiness.

Instead, the goal of a protection-oriented sale is to for the client to understand why they should pay more premium. Every dollar of premium beyond the bare minimum equates to less risk and greater certainty of outcome. A successful protection-oriented sale is one where the client feels confident that they’re going to get the coverage they need for as long as they need it – and that means, in almost every circumstance, paying more money than seems necessary based on the best-case scenario. Waiting to solve the problem is not an option. The non-linear nature of life insurance requires even small problems to be fixed immediately. If not, then small problems will always turn into big problems, and sometimes very quickly.

As protection-oriented sales come back into vogue, we have a chance to actually get it right this time by framing the sale around risk rather than cost. Whole Life policies aren’t expensive. They’re riskless. That’s the cost of completely removing the variables. Any policy with a premium less than Whole Life from a Big 4 mutual company requires that the client take on risk that they must intuitively understand and believe is worth the reward.

It’s a high bar of engagement and sophistication that very few clients will clear. If they can’t, then the goal is clear – sell them them the lowest risk product with the highest certainty of success, regardless of the price. Clients don’t care about and don’t even remember the price of the products you didn’t sell them. What they care about is having the coverage they need when they need it – and that’s the only measure of success.