#413 | The Option Tenor Conundrum

Author’s Note – Conundrum is the right term for this topic. Any time I write an article about option pricing, I feel acutely aware of the fact that most people who subscribe to this newsletter didn’t sign up to read about options. Unfortunately, there is no way to write about Indexed UL and not write about options. But this topic is particularly heady. I felt like I had an intuitive grasp of the math but I still had to work it over to get it to make sense. The good news is that there’s some easy intuition at work here – short-tenor crediting strategies are more expensive than long-tenor crediting strategies, which means their total upside and illustrated performance is lower. The technical reason has to do with the nature of volatility, as described in detail below, but the intuitive reason is that short-tenor strategies mean that any given return is less consequential than the returns in long-tenor strategies. A 0% return over one day is nothing. A 0% return over 5 years is an enormous problem. Risk/reward is at work and, as you’ll see below, the market actually handicaps the long-tenor strategies by how it prices implied volatility. So despite the fact that the optics of long-tenor strategies are more attractive, the more compelling case is actually to go short, maybe even as short as one month.

One-year crediting terms are so common in Indexed UL products that, these days, they’re almost taken for granted. It just feels like the most logical approach. People tend to think about returns in one year chunks. Advisors and clients meet on an annual basis. COI rates and other policy charge rates change on an annual basis. The Benchmark Index Account in AG 49 itself is a one year crediting strategy. One year crediting terms are nice, neat and easy – but they’re hardly the only way to do it.

One-year crediting relies on one-year options that occupy just one point on a continuous spectrum of potential option payoff periods, which are commonly referred to as tenors. At the short end of the tenor spectrum are zero-day options (0DTE) and the long end is 5-year options, although there are some bespoke solutions that can go longer. Theoretically, there is no reason why an Indexed UL product couldn’t credit interest in intervals as short as one day or as long as five years. If there’s a liquid option market on a strategy, then that strategy can go into an indexed insurance product.

Crediting strategy tenors greater than one year have been around for a very long time, but they really started to gain momentum in the mid-2000s prior to the enactment of AG 49 in 2015. AIG rolled out Elite Global in 2006 and it had a 5-year crediting strategy with a default illustrated rate of 10.28%. Voya had a similar structure with similarly aggressive illustrated rates. Both of those strategies used a combination of three indices, but PacLife had a pure 5-year S&P 500 strategy that illustrated north of 9%. There was a time, however brief, when it felt like long tenor crediting strategies might take over the Indexed UL world.

But it was not to be. AG 49 explicitly nixed the illustrated benefit of crediting strategies with tenors longer than one year. There was some back-and-forth about the relative merits of long tenor crediting strategies, but the reality was that it wasn’t the hill to die on for the Indexed UL writers. They had other things to worry about. And as a result, crediting strategies with tenors longer than one year ended up illustrating no better than one year crediting strategies. Since then, carriers have gravitated to using almost exclusively one year tenor crediting strategies.

Under AG 49, there is also no benefit for offering tenors shorter than one year – and yet Prudential did it anyway. The illustrated rate for the 6-month S&P 500 crediting strategy is 3.03%, which compounds to 6.15%, on a 6-month Cap of 4.25%. The default illustrated rate for the 1-year S&P 500 strategy with a 10.25% Cap is 6.42%. If you’re choosing the 6-month strategy then it’s because you like the story, despite the fact that it has a lower headline Cap, lower total annualized upside potential and lower annualized illustrated performance.

Option tenor hasn’t been a mainstream part of the conversation in Indexed UL since the adoption of AG 49, but Prudential Momentum IUL opens the door to the conversation. Imagine a product that offers three S&P 500 point-to-point crediting strategies with tenors of 1 month, 1 year and 5 years. Which one is best for a client? That’s a tricky question to answer. They all use the same index. They all use the same method of limiting the upside credit. The difference is in the frequency of the credit. What’s the value of an option tenor? To answer that question, we have to dig a bit into the oddities of option pricing.

Let’s start with some basic theory. Options are derivatives, not investments. The entire theoretical construct for option pricing hinges on the idea that value and cost must be connected. Black-Scholes makes this argument by saying that the price of any option is the expected value of its payoff. That’s true whether we’re talking about simple equity call strategies or complex, path-dependent, multi-temporal options like multiplicative cliquets. If there is more value, then there will be a higher cost.

Value in options is fundamentally derived from two things – interest rates and volatility. Interest rates are easy in that they tell us the neutral expectation of the return of the underlying asset. Volatility is the tricky bit. It’s the “insurance” component of the option. The more volatile the underlying asset, the higher the price of the option because of the potential for very high payoffs.

Volatility is quoted on an annualized basis. The S&P 500, for example, typically has annualized volatility of around 15%. Annualized volatility is not the same thing as daily volatility. Dividing annualized volatility by the square root of the number of trading days (252) yields daily volatility, which is 0.94%. That sounds pretty tame, right? But consider the fact that a 0.94% daily return equates to an annualized return of 969.74%. Yes, for real. A negative 0.94% daily return is equal to a negative 99.9% return. But, of course, the index has offsetting daily returns that create a much tamer annual return profile. In other words, there’s a lot of daily noise between the one year intervals that washes out for annual return calculations.

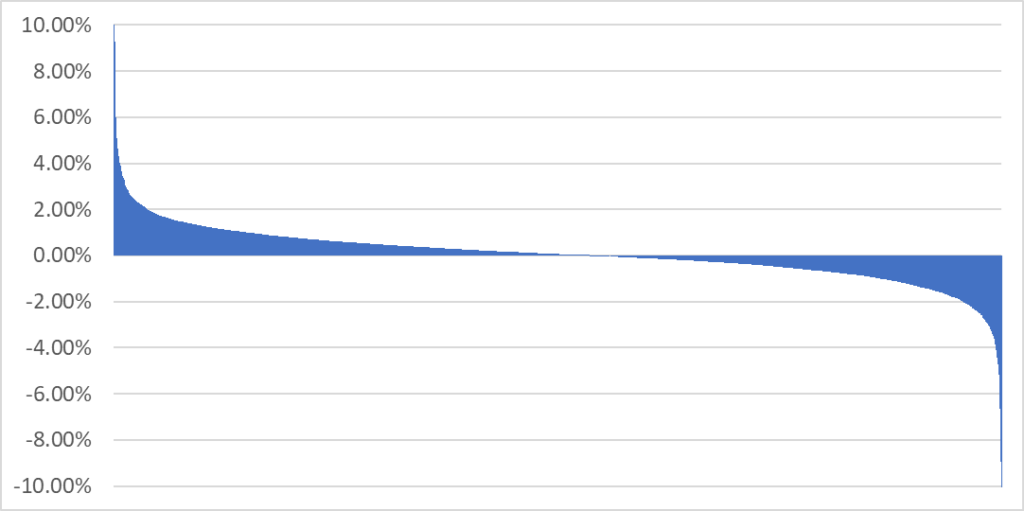

In fact, the daily noise is a lot larger in the real world than the figures above. The average daily return for the S&P 500 going back to 1997 is about 0.04% with a daily standard deviation of 1.2%. Check out the graph below showing daily returns in the S&P 500 ranked best to worst since 1997:

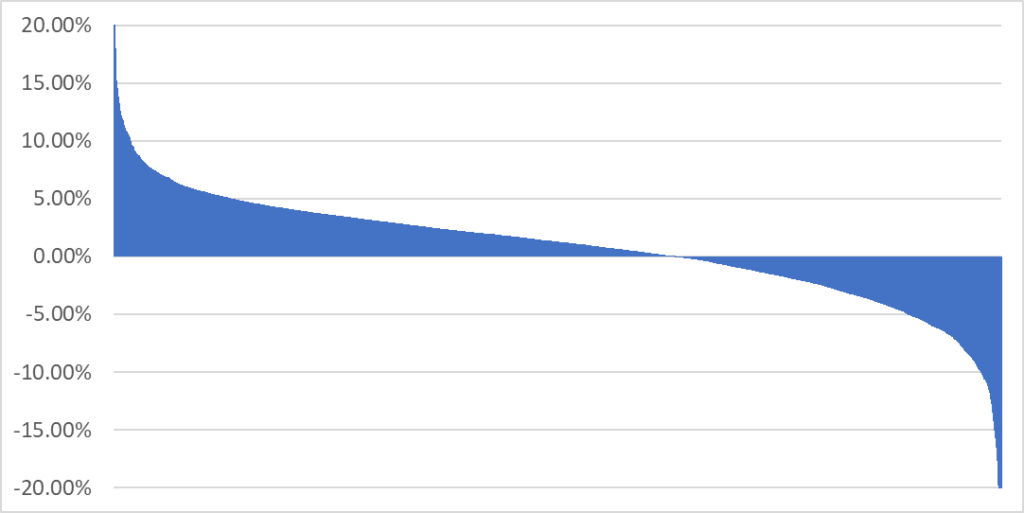

The same is true for monthly returns but obviously the effects are less extreme. Here’s the same chart as above but this time for monthly returns:

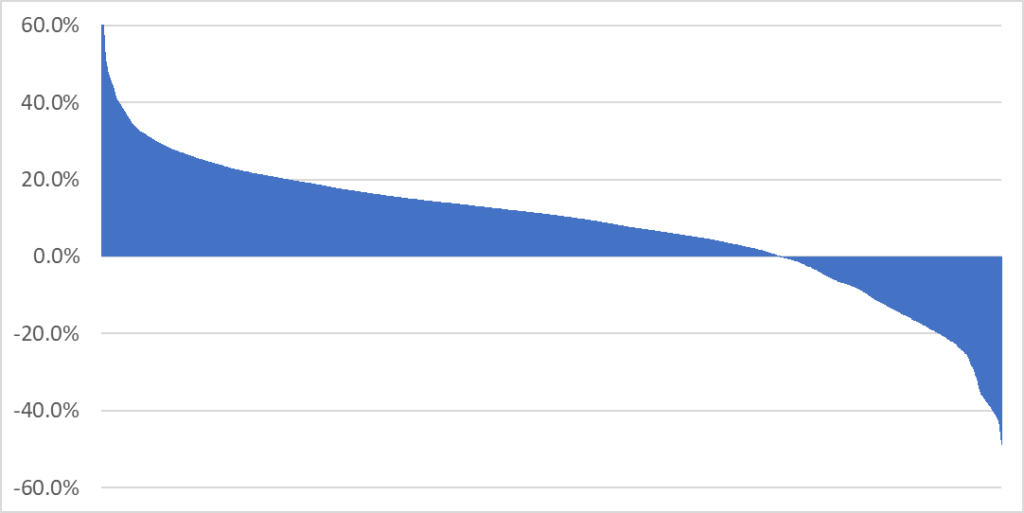

The numbers are bigger, but only because we’re talking about months rather than days. If we annualized a monthly return of 5%, which is the standard deviation for the monthly returns in the dataset, we’d get a total annual return of about 80% – high, but not completely insane like in the daily returns. Monthly looks a lot closer to annual than daily in terms of return and variance characteristics, but there is still a heck of a lot more variance than in annual returns, as shown below:

The opposite is true for crediting strategies with longer terms. For 5-year strategies, for example, the average return is 6.75% since 1997 but the annualized volatility is just 7.43%. Daily volatility catches (essentially) all of the noise. Monthly volatility catches 1/21th of the noise. Annual volatility only catches 1/252nd of the noise. And 5-year volatility? Just 1/1260th. A lot of index movements – noise – wash out if you’re only looking at the index every five years. Over that period of time, index returns start to look very stable and very predictable.

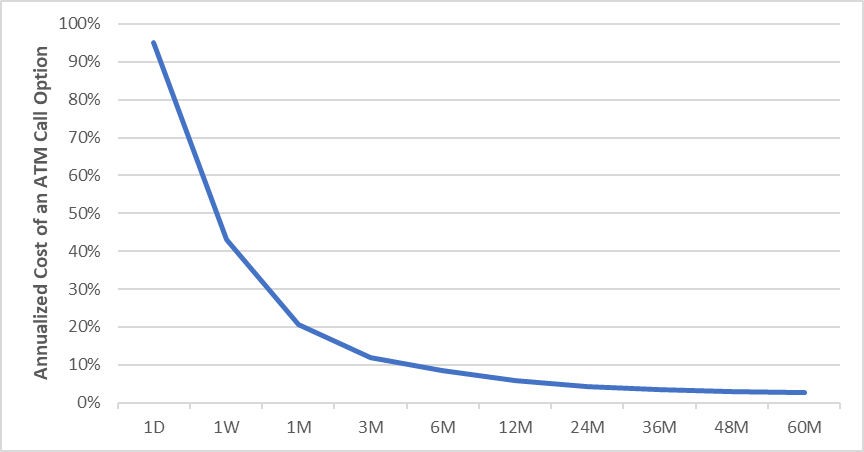

This volatility dynamic has profound implications for option pricing. Take a look at what it would cost to buy uncapped, at-the-money call options for an entire year at the intervals below using a 0% interest rate assumption, no dividends and a flat 15% annual volatility assumption for all tenors. To put this into context, a daily option means buying a new option every single day and totaling the cost of those purchases throughout the entire year. A 5-year option means buying exposure for 5 years but annualizing the cost back to one year.

Think about this for a second. All of these options use the same 15% annualized volatility assumption, but their pricing is wildly different. If you want to buy the upside on $100 of the index on a daily basis, you’re going to spend $95 over the course of the year to get it. But if you want upside exposure only on an annual basis, it costs you around 6%. If you’re willing to get upside exposure on the same $100 but over 5 years, the annualized cost is just 2.6%.

The difference is that even though the headline volatility of 15% is the same, that’s not how it translates to the price of the option. If you’re buying a daily option, the annualized return range that is being represented by 15% annualized volatility is -99.9% to nearly 1000%. For one month options, the annualized return range shrinks to -41% to 66%. For annual returns, it’s 15% and negative 15%, obviously. But for 5-year options, it converts to just positive 6% to negative 8%. The simple point is that 15% annualized volatility means something very different at different time intervals and, therefore, the annualized price of the options are vastly different.

So yes, it’s a wonderful theory that you could have a 0% Floor every day, but if you had a 5% option budget to spend for the whole year, then you’d get about a 5% daily participation in the moves of the S&P 500. That produces, on average, a 0.02% daily return with an average annualized return of about 5.5% – barely beating the option budget of 5%. Over the same period of time and using the same parameters to 1 year options, you’d get a whopping 9.66% return.

Longer crediting strategies post even bigger numbers. If you took that same pricing and pushed the crediting period all the way out to 5 years, you’d get even more leverage with a participation rate a little over 185% because fo the lower annualized cost of the option. Apply that to the historical data and the average backtested annualized return is over 12%. Extending the length of the crediting strategy seems like a no-brainer by every performance metric.

There are, however, two countervailing forces. The first is intuitive. Extending the term of the crediting strategy means a greater impact of any individual credit. There are 252 trading days in the year. Given the fact that the participation rate (based on the math above) is about 5%, then no single day is going to swing the annual return by a huge amount and, on top of that, the number of positive and negative returns throughout the year will be fairly consistent. Since 1997, the S&P 500 has delivered 47% negative daily returns and 53% positive daily returns. You just need to be right more than half the time to end up in the black because you’re getting so many opportunities.

That’s not the case with a 5-year crediting strategy. A negative return over 5 years is a catastrophe in terms of overall lost opportunity. The original AIG Elite Global was illustrating a 10.28% annualized crediting rate over each 5-year period, which equates to total interest of 63%. However, thanks to poor performance in all 3 index constituents of the global look-back crediting strategy, policyholders instead received a 0% credit for the first 5-year credit. The loss of interest isn’t 3.9 basis points, which is the equivalent daily interest or even 10.28% for a true one-year crediting strategy. Instead, the loss is the full 63%.

Since 1997, the S&P 500 has negative returns over 31% of 5-year periods, more than the incidence of negative returns over 1 year periods (25%) and just behind the incidence of negative returns over 1 month periods (36%). One month of 0% is no problem. One year of 0% is something to watch. But 5 years with nothing to show for it? That’s a material and potentially insurmountable problem that has never been replicated in consecutive annual S&P 500 returns. The wins are bigger in long-tenor crediting strategies, but so are the losses.

The second countervailing force is that the market prices volatility across terms very differently. Theoretically, volatility should be priced the same for all option tenors. All of the options, after all, are based on the same index. But anyone with even a passing knowledge of the options market knows that’s not how things work. Option pricing formulas such as Black-Scholes do not determine the price of options – they interpret the option prices that are observed in the market. Because all of the other option pricing factors are known, the pricing mechanism for the option is volatility – specifically, the implied volatility based on actual option prices. Actual market-clearing option prices determine implied volatility. The dog wags the tail, not the other way around.

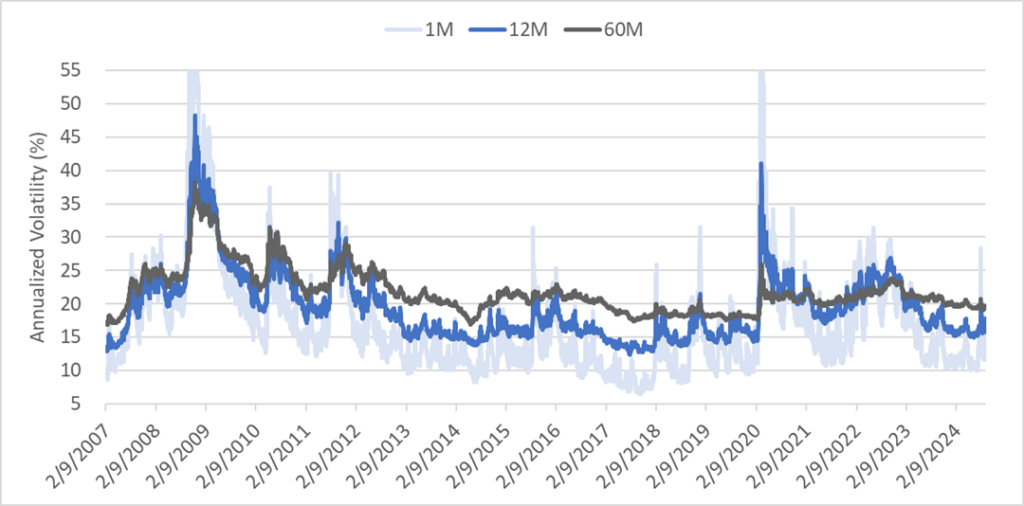

The interpretation of implied volatility is that it is the market-priced volatility over the term of the option. Because options have different terms, it makes perfect sense that they’d also have different implied volatility. Short-term options, as you can imagine, have very volatile implied volatility. The VIX is a classic example of short-term volatility dynamics. When the market falls, VIX pops. Why? Because VIX measures 30-day implied volatility. One year volatility moves more slowly and less dramatically than the VIX. 5-year volatility is practically immobile by comparison. Take a look at the implied volatility for 1-month, 1-year and 5-year options since 2007:

The other thing you’ll notice pretty clearly is that short-term implied volatility is lower than long-term implied volatility. Median implied 1M volatility is 14.77% and median 1Y implied volatility is 18.19%, but median 5Y implied volatility is 21%. The average are a bit tighter – 17%, 19.5% and 21.8%, respectively – due to the fact that short-term volatility responds more quickly and dramatically to index declines.

The fact that longer-term options have higher implied volatility makes them, all things being equal, more expensive than shorter-term options. That cuts into the perceived advantages of long-term crediting strategies. In fact, there is a cottage industry dedicated to selling options for the simple reason that implied volatility at all of these durations is higher than realized volatility, but particularly for long-term options. Think about it – if you could just buy 5-year options rather than owning the index and pick up a huge performance advantage, wouldn’t everyone do it? Of course. Why, then, does essentially no one do it? Because the market structure has already eliminated the advantage through the price of the option. That’s exactly what you’d expect to see in a properly functioning market*.

For all of the perceived advantages of long-term crediting strategies, the reality is that the cards are stacked against them. They offer more upside but also the risk of catastrophic outcomes and most policyholders don’t have enough time to ride out the cycles. They’re structurally cheaper because the effective volatility is lower, but the actual implied volatility is higher and that’s what counts. There was a time when long-term crediting strategies could illustrate better annualized returns than annual crediting strategies and, thankfully, AG 49 put a stop to that with very little protesting from Indexed UL writers. Part of the reason, I think, is that they knew it was indefensible. Had they gone too far down the rabbit hole of defending long-term crediting strategies and they might have imperiled the whole franchise as the arguments got more and more nonsensical and circular. Better to cut their losses and move on.

One-year strategies, from my vantage point, really are the sweet spot. They’re long enough to get the potential for real upside, but short enough for any client to have plenty of time to recover from missed credits. They pay an implied volatility penalty, to be sure, but the market is deep enough to provide fair pricing and plenty of liquidity. And, of course, it’s a nice cadence that matches up to the annual statements provided by insurers. Sometimes the status quo is the status quo for a reason.

One of the bizarre things about Indexed UL (and FIAs) is that value is measured by backtests, not by actual option pricing dynamics. This sort of backtesting is completely unique to fixed indexed insurance products and is found literally nowhere else in the financial world. Backtesting is built to be gamed and therefore leads to some bizarre, inaccurate and internally contradicting results. If we were relying solely on backtests feeding illustrated performance, which is what illustrations would do without AG 49, then long-term crediting strategies would still be proliferating in Indexed UL products the way that they have in Fixed Indexed Annuities**.

Prudential’s Momentum IUL has opened the door to the opposite question – how short can an indexed crediting strategy go? Could we see a carrier even doing monthly index credits? I think it’s possible. Monthly index credits would provide more stability and consistency of returns over time without giving up too much upside potential or illustrated performance. It’s an interesting middle ground between fixed and indexed crediting that lines up nicely to monthly policy charge processing while playing in the more efficient part of the option market.

Innovation in Indexed UL, for too long, has been about maximizing illustrated performance. Shorter option tenors don’t deliver illustrated performance, but then can deliver different stories for clients that revolve around the fundamental Indexed UL value proposition of upside potential and downside protection. It’s about time someone gave it a shot – and I doubt Prudential will be the last.

*Not to belabor a point that I’ve already discussed many times in this publication, but this is the core problem with the concept of “option profits.” Folks who believe in structural option profits are letting the tail wag the dog. They read the Black-Scholes formula as a literal determination of the price of the option. It’s not. Black-Scholes provides a framework for interpreting market-clearing prices. If realized volatility equaled implied volatility, then there could be structural options profits, but that’s never the case. Implied volatility is always greater than realized volatility, which means that the higher price of the option eats into the perceived “option profits.” The degree to which that happens is up for debate, but here’s what’s not up for debate – if minimizing the gap between realized volatility and implied volatility is the goal, then carriers should be trading short-term options, but they don’t. Why not? Because there is a canon of well-documented literature showing that selling short-term options is profitable. If selling short-term options with low implied volatility is profitable, then why would anyone think that selling long-term options with high volatility is not profitable?

**That’s currently the case in FIAs and it has turned into a real problem. Nationwide, for example, sold two variants of its massively successful New Heights FIA product – one with 2 year crediting strategies and one with 3 year crediting strategies. Which one sold better? You guessed it, the 3 year. It illustrated better and, presumably because the options were cheaper, it also paid higher overrides to IMOs. Nationwide sold billions of it and now clients are getting 0% credits in consecutive 3-year crediting strategies. The problem has become so acute that Nationwide has added 1 year crediting strategies to in-force contracts.